Portfolio Update 07. Apr 2022

Portfolio Update 07. Apr 2022

Stock market indices lower, second month of Russia-Ukraine war, central bank interest rates higher, energy and food prices higher, countries pursuing their energy and food security

In April we saw the major US equity indices lower (S&P 500 -9.18%, Nasdaq -13.63%), with growth underperforming value while energy and commodities holding up. US and UK central banks have increased their interest rates to 1.00% while official inflation numbers are at 8.50% in the US, 7.80% in EU and 7.00% in the UK. Inflation currently seems to be driven by higher energy and food prices and the west's sanctions against Russia are only expected to make it worse, which is a bit ironic as sanctions don't seem to be hurting Russia 1.

Russia-Ukraine war is on its second month and Russia's forces seem to have changed their area of focus to the South-East of Ukraine. We see most of the western countries united in their sanctions against Russia which seems to be causing more damage to themselves. At the same time however we're seeing many other countries not fully aligning with the west, making their energy and food independence a higher priority, working closer with Russia to secure cheaper energy.

What we're witnessing is an attempt by countries not fully aligned with a US centred west world, mainly lead by China and Russia, to establish a new world order that suits them better. Having studied history we know that when empires get challenged they scarcely just give up their dominance but they fight as hard as they can, simply because they don't have another choice. US’ global hegemony is currently challenged and we don't think it will let it go easily. How this will end we can't possibly know, but we believe we'll see more hot wars in the future, either direct or proxy wars in an attempt to undermine the sovereignty of Russia and China (Baltic states, Kazakhstan, Georgia, Taiwan, etc).

We expect to see more political instability in countries that dissent from the western line (e.g.: Pakistan's Imran Khan was ousted on the 10th of April after trying to get closer to Russia 2, Solomon Islands sign security pact with China 3) and more countries dissenting (e.g.: Hungary, Serbia and others not wanting to impose sanctions against Russia).

We are also witnessing increased dissatisfaction among citizens against their governments' policies and as energy and food price increases hit more households, we expect to see more protests. We don't see governments having many options, either they'll need to find cheap sources of energy fast and keep their voters happy, or they'll have to get more authoritarian to control opposition. We wouldn't be surprised to see some kind of event — maybe another pandemic, a cyber attack, a terrorist attack, etc — that allows governments to impose more emergency laws or even martial law.

This is a long intro but we're more confident than ever that all these structural trends are highly inflationary and we believe ‘The Haptón Portfolio’ will perform well in the next 5+ years. Short term volatility is also expected (which we could dampen by increasing our exposure to physical commodities rather than just producers, e.g.: Sprott Physical Uranium Trust Fund (U-U.TO), physical precious metals funds, etc), but we're OK with that and we 'll try to deploy capital in every dip. The current dip in commodity producers share prices might prove to be a good entry point or an opportunity to deploy some more capital.

In closing, we loved the following podcasts and we believe they're worth listening to:

MacroVoices #321 Ole Hansen: The Commodity Supercycle Has Begun

Superinvestors and the Art of Worldly Wisdom, “Diego Parrilla On The Three Levels Of The Investment Game”

Performance

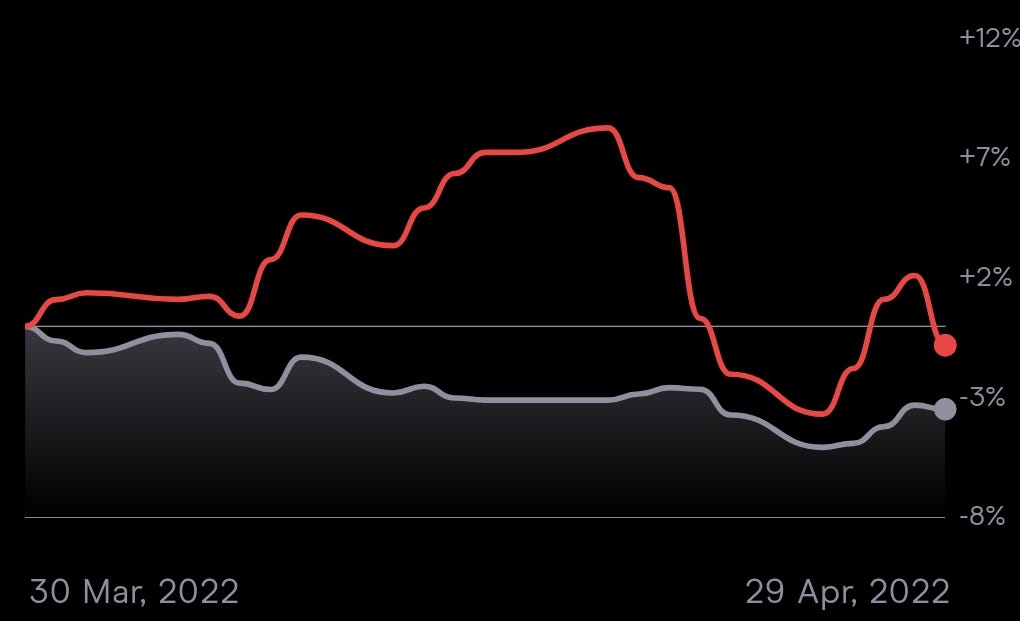

For the month of March 2022 ‘The Haptón Portfolio’ had a +0.46% Money-weighted rate of return (MWRR) and a -0.77% Time-weighted rate of return (TWRR).

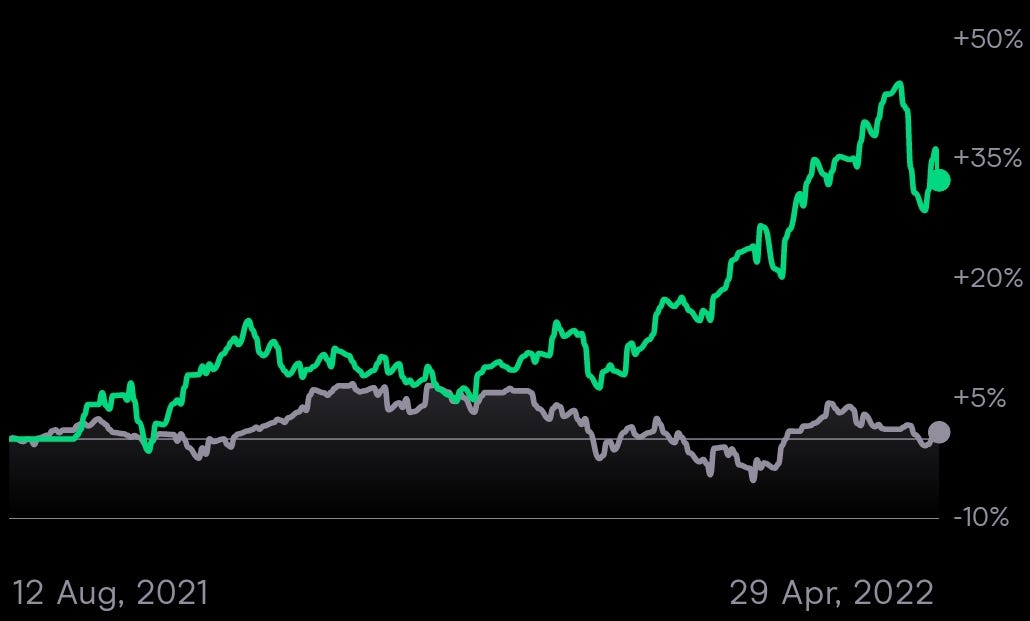

Since inception (end of August 2021 to end of March 2022), MWRR was +37.01% and TWRR +32.50%.

Monthly performance vs Benchmark

For the month of March 2022 the portfolio's performance was -0.77%, outperforming the benchmark index by +2.71%.

TWRR for March; -0.77%

Benchmark Index “FTSE All World ETF (£VWRL)” TWRR for December; -3.48%

Performance Since Inception vs Benchmark

Performance since inception (since the 31st of August 2021) was +37.01%, outperforming the benchmark index by +36.20%.

TWRR since inception; +37.01%

Benchmark Index “FTSE All World ETF (£VWRL)” TWRR since inception; +0.81%

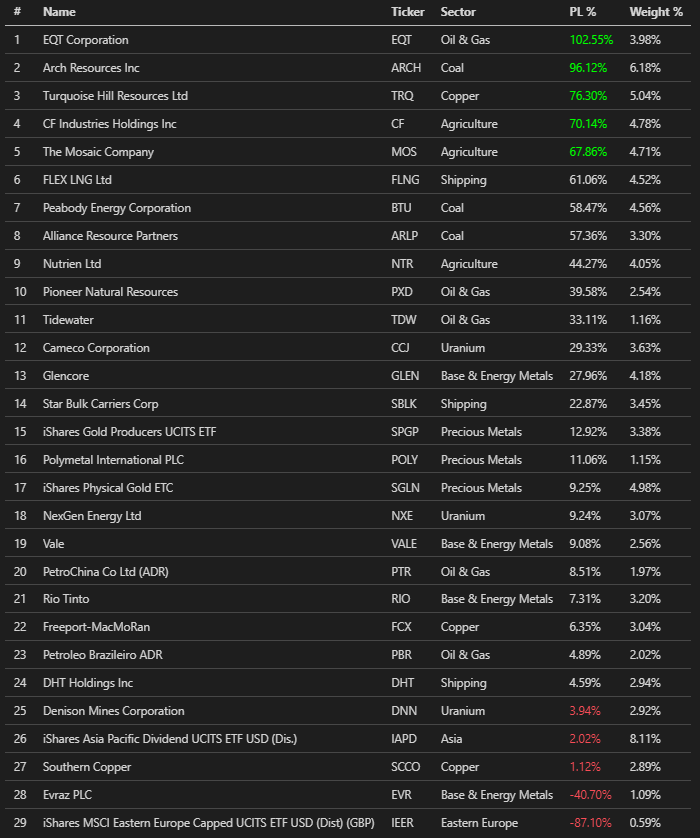

Positions

Active

Liquidated

Closing Thoughts

We're happy with the portfolio's performance so far and we're getting ready to deploy some more capital, potentially even initiating some new positions in the next couple of months. We'll keep you updated.

Watchlist

Nothing new in our watchlist for this month.

Disclaimer

We are not professional financial advisors, therefore not qualified to give financial, investment or any other kind of advice. The content in our “The Haptón Portfolio” publication is intended to be used and must be used for informational purposes only. It is important you do your own research and seek independent professional advice before making any investment decisions.

Disclosure

We hold investments in the companies mentioned in “Figure 3”. We may initiate or close positions without further notice.