Portfolio Update 05. Feb 2022

Portfolio Update 05. Feb 2022

Ukraine-Russia war, energy, portfolio resilience, War Inc.

We never thought we'd experience another war in European soil, yet here we are. On the 24th of February 2022 Russia launched a large scale military attack (invasion, military operation, call it however you like) in Ukraine. Since then we've seen escalations in both sides, with the west imposing more sanctions to Russia while sending more arms to Ukraine, and Russia keep advancing deeper into Ukrainian territory. We have no idea how this situation will be resolved but we need to be prepared nonetheless.

Apart from the obvious horrors of war, we can't really see how inflation won't be in our lives for the next few years. Cutting off a country like Russia that is a supplier of cheap energy, fertilizers and grains to the world and especially to Europe, means that the price of these goods go up. This is going to be a much bigger problem for European countries rather than China which will keep trading with Russia, or the US which has less dependence on Russian trade.

This won't be an issue however, if the energy, fertilizers and food required come from somewhere else. However we don't see where this new supply will come from, especially after western oil and gas majors have been and still are reluctant to invest in new projects. It is looking more and more probable that energy and food prices, especially in Europe, go much, much higher. Restoring trade with Russia would solve some of these issues but we're not very optimistic about it. Time will tell.

Portfolio Resilience

One of our core principles when building “The Haptón Portfolio“ is that we can't possibly know nor predict how things will unfold in the short term, but we can make educated guesses based on longer term structural trends. By constructing a portfolio with adequate risk management, we should be able to take advantage of these trends while protecting ourselves from the potential downsides.

For reasons explained in previous publications we see structural issues in the energy, materials, agriculture and shipping sectors. We believe these issues will take years to be resolved, as it will require a change of sentiment by the populations and the ruling classes. Inflation is painful, but probably necessary to help humanity prioritize what's important and what's not.

Let us explain our rationale when constructing “The Haptón Portfolio” with an example.

We believe that humanity will need energy in the future. That energy needs to come from somewhere. Will it come from oil, natural gas, uranium, coal or renewables? We can't possibly know. Unless it comes from a source whose existence we are unaware of, then even in the possibility that all these sectors go bankrupt, one of them will benefit and will probably make up for our losses incurred in other sectors, since most capital will flow into it.

Of course this is a very simplistic argument and one could counter argue that technology and innovation will somehow provide us with cheap energy. Currently we haven't seen such an innovation that can be mass produced and deployed worldwide, solving the issues that we're facing at the moment. Eventually we believe this to be true and technology and innovation will allow humanity to have cheap energy. Until then we need to invest accordingly.

With a similar rational we invest in companies within a sector. We try to be as globally diversified as possible, invest in companies that make sense and avoid the ones that don't. For that reason we've invested in Russian, Eastern European equities and Chinese companies. We don't always get things right but we try to stack the odds in our favour.

This brings us to Russia and how, after escalating sanctions from the West, Russian companies became uninvestable. We didn't sell our Russian companies even though we could have and in hindsight “should have” as it was “obvious”. But we don't regret it because it was, and still is a risk we're willing to take.

Which brings us to portfolio resilience.

Overall, even though we've seen our Russian and Eastern European positions lose 50%, 60%, 90% of their market value, our portfolio not only held well but it continued outperforming the benchmark index, as well as the broader market indices. This highlights the resilience of this strategy (or we're simply fools of randomness). Whether this strategy will continue working, once again only time will tell.

Performance

Let us look at the performance of “The Haptón Portfolio” in more detail.

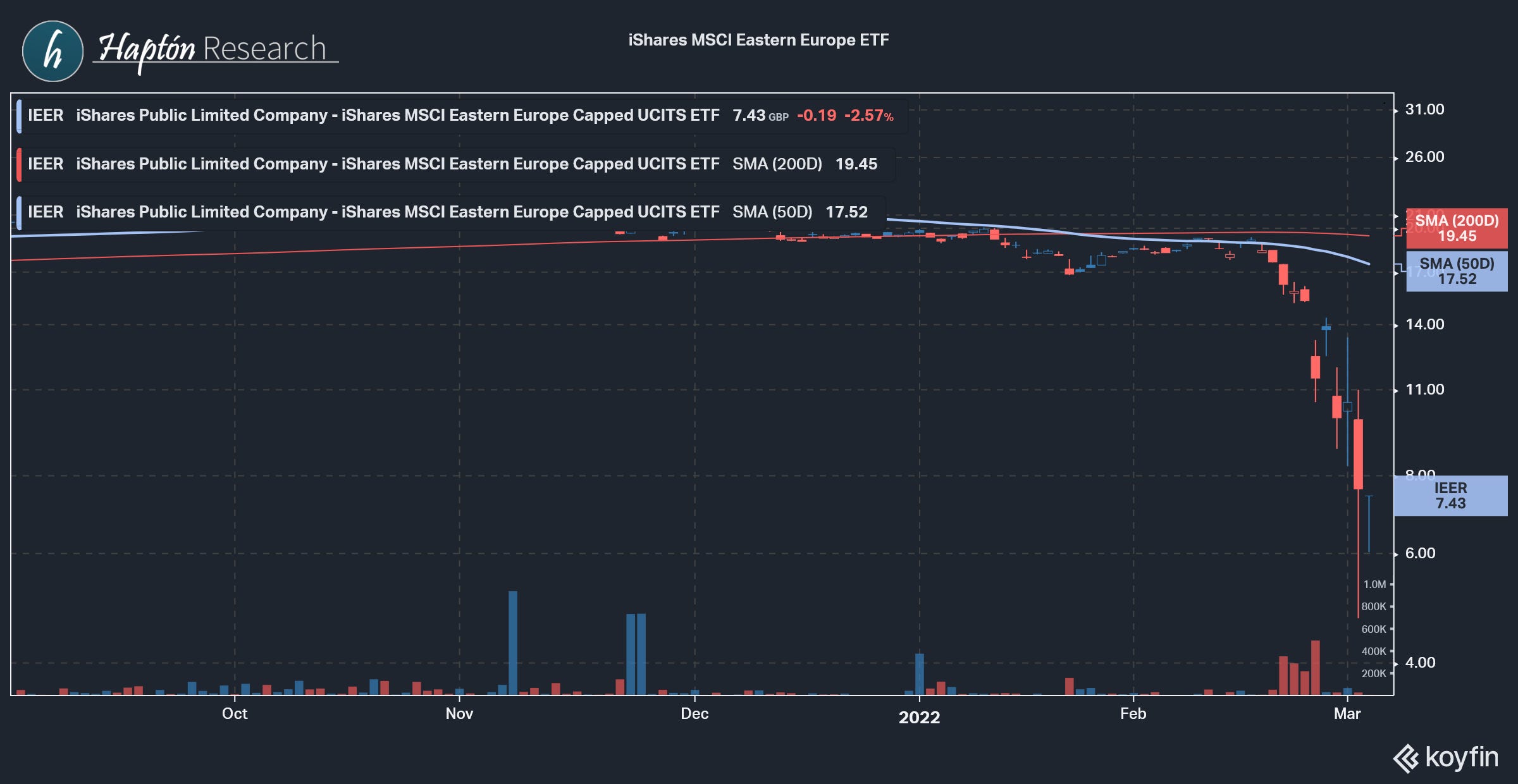

Last month, before the war in Ukrainian, our exposure to Russia and Eastern Europe was 8.44%. After the war started and western governments started imposing sanctions to Russia, our Russian equities lost most of their market value.

At the time of writing our exposure to Russia and Eastern Europe is around 3.77%. EVRAZ has lost almost 90% of it's value and Eastern Europe ETF has lost just over 60%.

Check the charts below, they look absolutely horrible!

But how did our portfolio perform overall, keeping in mind that most market indices have been trending lower as well?

F or the month of February 2022 “The Haptón Portfolio” had a +10.05% Money-weighted rate of return (MWRR) and a +5.51% Time-weighted rate of return (TWRR).

Since inception (end of August 2021 to end of February 2022), MWRR was +19.64% and TWRR +17.90%.

Monthly performance vs Benchmark

For the month of February 2022 the portfolio's performance was +5.51%, outperforming the benchmark index by +8.01%.

TWRR for February; +5.51%

Benchmark Index “FTSE All World ETF (£VWRL)“ TWRR for December; -2.50%

Performance Since Inception vs Benchmark

Performance since inception (since the 31st of August 2021) was +17.90%, outperforming the benchmark index by +19.06%.

TWRR since inception; +17.90%

Benchmark Index “FTSE All World ETF (£VWRL)“ TWRR since inception; -1.16%

Positions

Active

Liquidated

We haven't liquidated any positions this month.

Closing Thoughts

So as you can see our Russian and Easter Europe positions are significantly lower, however looking at this in the context of the overall portfolio we've done exceptionally well.

We will not be closing our Russian or Eastern European positions. We will be placing another tranche of investment this month (March 2022) and we will try to add to these positions assuming we're allowed to do so.

We consider these Russian and Eastern European positions to be extremely risky and the chances their worth will be 0 very probable. So if you're not comfortable with investing money that you will probably lose for the extremely low probability that you will be compensated many times more, then you shouldn't invest in Russian or Eastern European equity.

We are also looking to initiate position(s) to oil service companies that should benefit by increased investment to oil and gas.

Watchlist

Tidewater Inc

We're looking to add Tidewater to our Oil & Gas exposure, as we think it will benefit from more investments flowing to new Oil & Gas projects.

From Yahoo! Finance (TDW);

Tidewater Inc., together with its subsidiaries, provides offshore marine support and transportation services to the offshore energy industry through the operation of a fleet of marine service vessels worldwide. It provides services in support of offshore oil and natural gas exploration, field development, and production, as well as windfarm development and maintenance, including towing of and anchor handling for mobile offshore drilling units; transporting supplies and personnel necessary to sustain drilling, workover, and production activities; offshore construction, and seismic and subsea support; geotechnical survey support for windfarm construction; and various specialized services, such as pipe and cable laying.

War Companies

As Smedley D. Butler once wrote “War is a racket”1. We believe many US companies will benefit by the current war in Ukraine and its second order consequences (European countries such as Germany rearming themselves). We don't think it's improbable for US defense companies to perform as well as vaccine manufacturers have performed during the COVID-19 pandemic.

That being said, we are not and will not be investing any of our capital in any companies directly involved and benefiting from war, so we're only present these as an educational example of first-order consequences of the military conflict in Europe.

We leave it up to you, your morals and ethics to decide whether you invest or not.

Invesco Aerospace & Defense ETF

From Yahoo Finance (PPA);

The fund generally will invest at least 90% of its total assets in the securities that comprise the underlying index. The underlying index is composed of common stocks of companies that are systematically important to the defense sector and are involved with the development, manufacture, operation and support of U.S. defense, military, national/homeland security, and government space operations. The fund is non-diversified.

Parts of the index are Raytheon Technologies Corp (RTX), Lockheed Martin Corp (LMT) and Northrop Grumman Corp (NOC).

Thank you for reading. Until next time, happy investing and good luck!

P.S.: If you liked this post, please like it and share it! It means a lot to us!

Disclaimer

We are not professional financial advisors, therefore not qualified to give financial, investment or any other kind of advice. The content in our “The Haptón Portfolio“ publication is intended to be used and must be used for informational purposes only. It is important you do your own research and seek independent professional advice before making any investment decisions.

Disclosure

We hold investments in the companies mentioned in “Figure 5“. We may initiate or close positions without further notice.